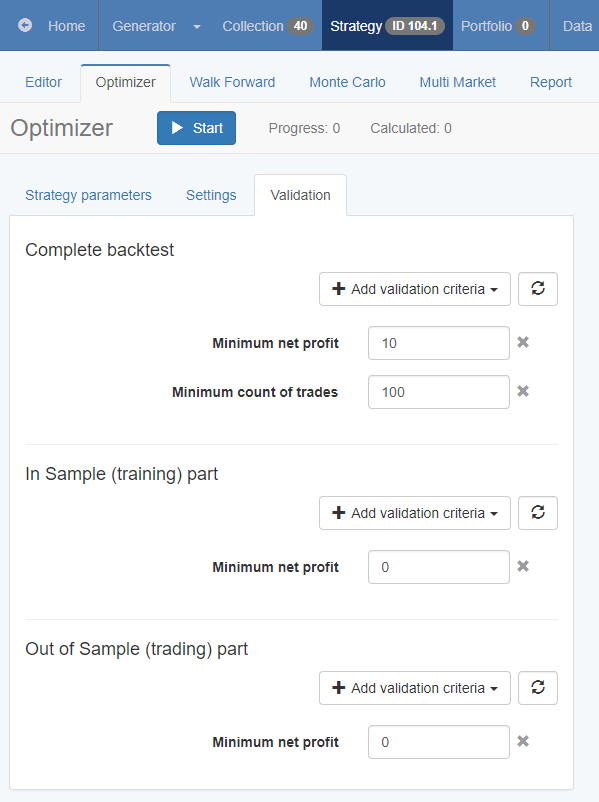

Popov, thank you, but it would be VERY important (to me at least) that the extra acceptance criteria for the Optimizer also has 3 parts: Complete Backtest, in sample, out of sample, like the normal acceptance criteria for the generator (and how it was before for the optimizer too). So that if selecting "10% OOS" for the optimizer in the reactor or directly within the optimizer, we can specify for example "at least 95 R-Squared for the COMPLETE backtest, but also at least 80 R-Squared for the 10% OOS part", then begin the optimization. I have always used this to find strategies that are overall stable, but ESPECIALLY stable in the last years (the 10% OOS). This option is not possible anymore now, having just 1 set of acceptance criteria for the whole backtest (or IS, as the optimizer will ignore the OOS part now and we can set now minimum values for the OOS part anymore during an optimization), which is a pitty :-(

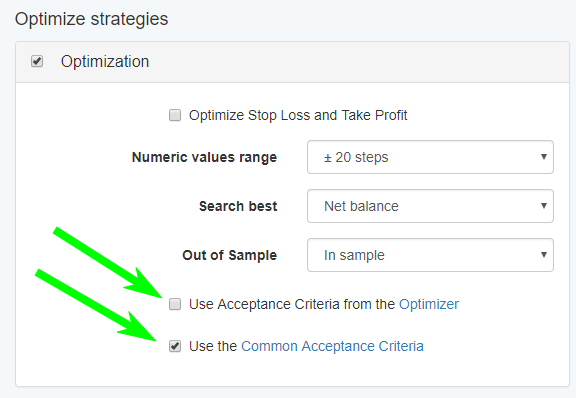

I´ve awlays used the optimizer this way: set it to 10% OOS, set the acceptance critera for the 10% OOS to at least a R-Squared of 80, then optimize the IS part for maximum R-Squared value, this isn´t possible anymore now and basically breaks my complete workflow of how I´ve created my good strategies :-(

I think it would be better if you´d simply add a second set of criterias in the settings page and then, in the Reactor / Generator / Optimizer, we can select "criteria set 1" for the generator, and "criteria set 2" for the optimizer, or use "criteria set 1" for both if we don´t need different acceptance criteria. Both "criteria set 1" and "criteria set 2" would have acceptance criteria for the complete backtest, for the IS and for the OOS part. If you can´t do that, can you please bring in the 3 split-parts into the Optimizer directly as well again (complete backtest, IS, OOS). That would be higly important to me as I am stuck now with only having 1 set of criteria for the Optimizer.

On large data-sets that is a real problem, because optimizing for a high R-Squared for the complete backtest can sometimes result in great first 28 years, but bad last 4 years (as I use 32 years of data). When we had the option to optimize the IS part for maximum R-Squared (or whatever) but FORCE at least a R-Squared of 80 in the 10% OOS part, the optimizer found great strategies that would be very stable overall and not just 28 years and then go down sligthly like it often is the case after 2015.

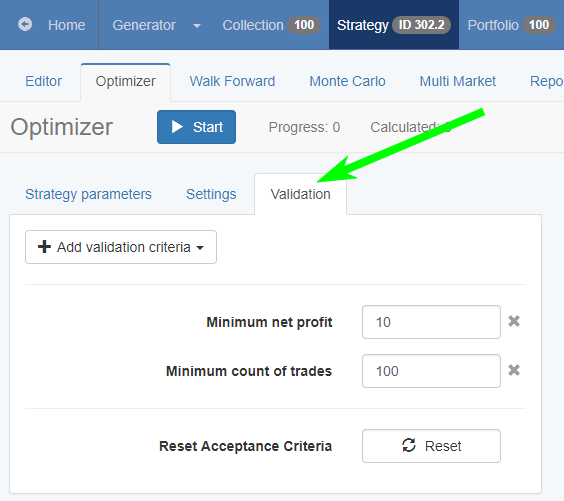

If using the new optimizer now, I have no way to set which minimum criteria to have in the 10% OOS. If I set it to 10% OOS now, the optimizer will only care about the IS and will completely ignore what is going on the in 10% OOS. Previously, the optimizer would also only optimize the IS part, but we could set that in the 10% OOS, it should at least have 100 trades, or at least return/drawdown of 10, or a R-Squared of 80, or whatever. Now it does absolutely not care anymore what happens in the last 10% of the backtest and just optimizes the IS part, regardless of what happens in the 10% OOS part. And that is a real problem at least for me, as I can´t optimize the way I´ve optimized anymore.

So summarized:

- Please bring back the option to use separate critera for the complete backtest, IS and OOS in the Optimizer instead of just 1 set of acceptance criteria.

Thank you so much!!!