Hello everyone,

I’ve noticed a recurring pattern, both from personal experience and various discussions in this forum. We all know how easy it is to generate a strategy with a visually perfect equity curve in Expert Advisor Studio (EAS). We go out of our way to use Out of Sample (OOS), Walk Forward Analysis (WFA), and various strict filters within the software.

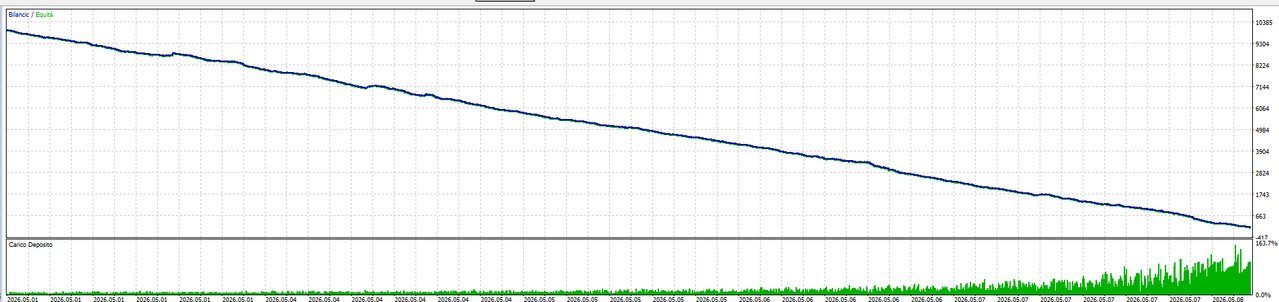

However, the main issue often remains the same: Not all strategies that pass these filters and make it into the Collection manage to survive (print a positive profit) when actually tested on a Demo or Live account.

Many people suggest testing the strategy on a Demo account for 3 months (as an example timeframe) before moving to a real account. But let's be more pragmatic: Why should we waste 3 months of real-world time purely just to wait for Demo results?

Wouldn't it be much more efficient if we "extend" the historical data and simulate the forward test instantly using a method I call "Blind Holdout" ?

The Critical Difference: EAS Built-in OOS vs. Blind Holdout

Many of us fail because we assume the OOS in EAS is the final test. In reality, when we enable the OOS feature (e.g., 30%), EAS still uses that OOS data as a selection criterion. If a strategy fails in the OOS zone, the engine discards it. This means the strategies in the Collection have indirectly been "optimized" to coincidentally fit that specific OOS data (Data Snooping Bias).

To overcome this, we need Blind Holdout Data—a segment of data that we completely hide and entirely exclude from EAS during the generation process.

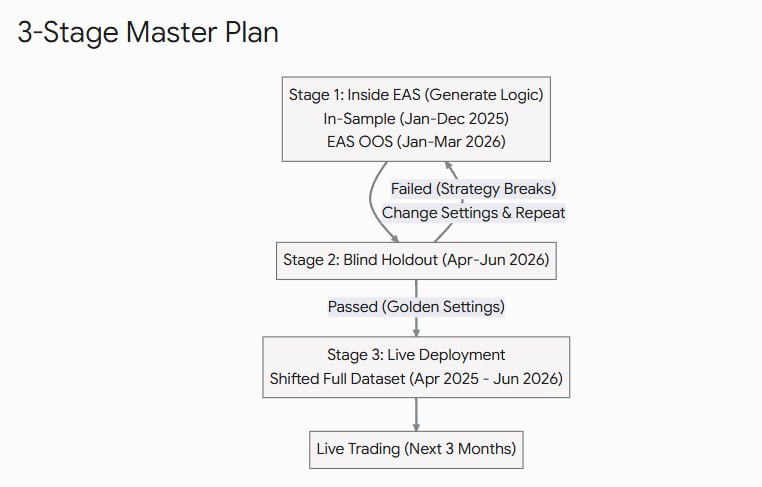

The 3-Stage Master Plan:

Here is the logic on how we can use a Blind Holdout not just to find strategies, but to validate the EAS Settings themselves. Let’s assume today is July 1, 2026, and we have data from January 2025 to June 2026.

Stage 1 (Inside EAS - Finding the Logic): We restrict the data loaded into EAS only up to March 31, 2026.

- In-Sample: Jan 1, 2025 – Dec 31, 2025 (The engine builds the logic).

- EAS OOS: Jan 1, 2026 – Mar 31, 2026 (The engine filters passing strategies).

(Note: In Stage 1, you can fully utilize the Reactor with all its analysis tools like Multi Market, WFA, etc.).

Stage 2 (Blind Holdout - Validating the Settings): April 2026 – June 2026 (3 months).

- We manually re-backtest the Stage 1 strategies over this last 3-month range (data the engine has never seen) by adjusting the Data Horizon and using the Recalculate button in EAS. If the strategy breaks down, we change our EAS Generator Settings and repeat Stage 1. We keep doing this until we find the EAS Settings that consistently produce strategies capable of surviving this Stage 2 Blind Holdout.

Stage 3 (The Ultimate Goal - Live Deployment):

- Once we find those "Golden Settings", we no longer need the Blind Holdout. We simply run EAS using these proven settings on the forward-shifted dataset (April 2025 up to yesterday, June 30, 2026).

- Assumption: Because the settings themselves have been rigorously validated through the Stage 1 & 2 holdout process, we can confidently assume that any strategy generated today will print positive profits for the next 3 months on a Live Account.

The Goal of This Discussion:

Based on this premise, I want to open a discussion:

"We need to figure out what kind of EAS Settings ensure that when the engine generates a strategy, that strategy consistently prints a positive profit when exposed to a Blind Holdout period."

My question focuses purely on EAS Settings. For those of you who have successfully formulated a robust engine setup—where your generated strategies rarely break down during forward testing—I truly hope you’d be willing to share them. Specifically regarding:

- What Acceptance Criteria do you use?

- What Timeframe do you use?

- How many Data Bars or what Date Range do you use?

- What preset indicators do you allow the engine to use initially?

- What specific "Strategy Properties" or "Generator Settings" do you use?

(Or you can directly upload your EAS Settings .json file).

Hopefully, by sharing these settings, we can formulate the "Meta Settings" for EAS that are truly reliable and massively save our research time.