I agree with Sleytus (Steve)

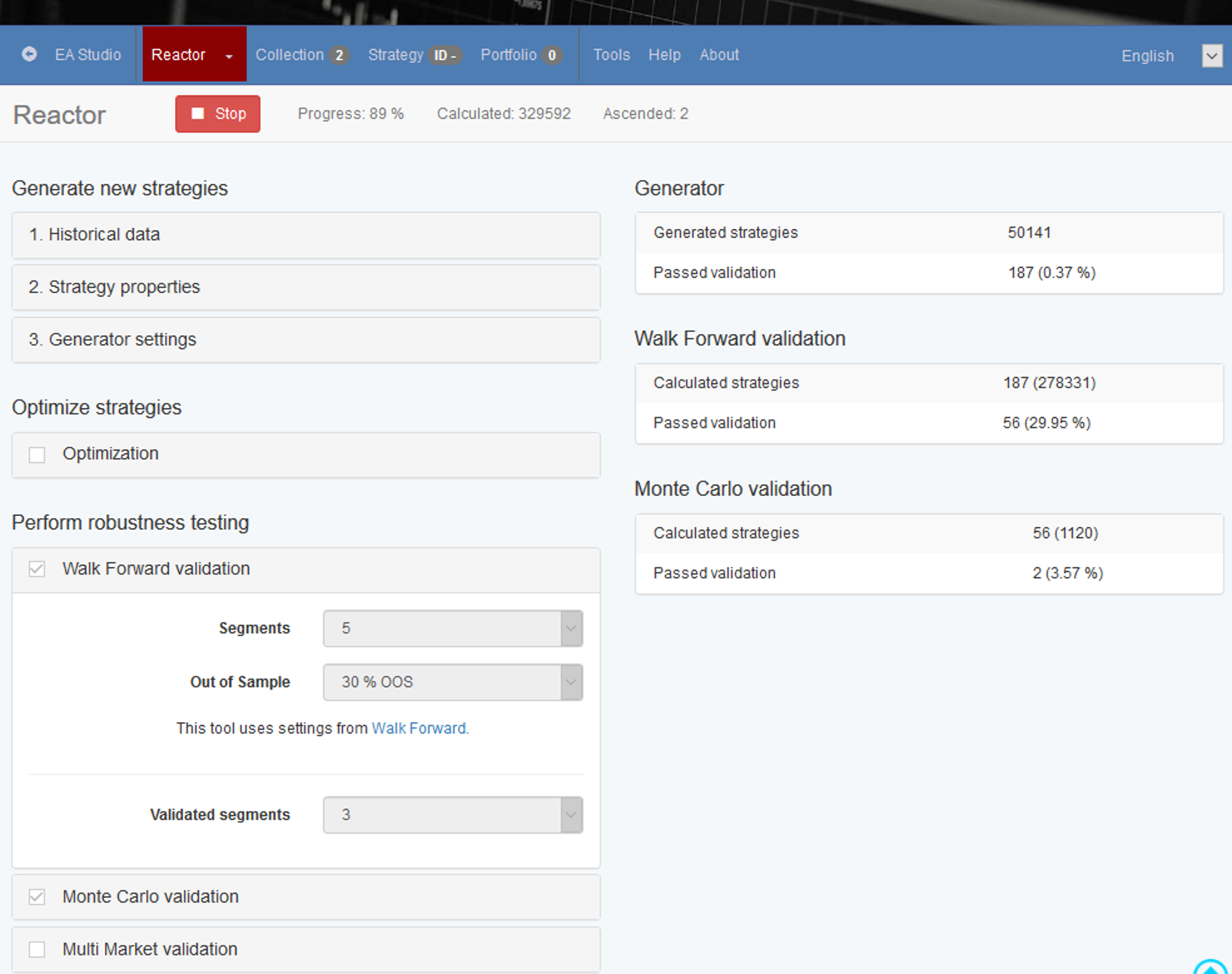

I question the value of Walk Forward. I'm not saying it has no value at all but I'm asking myself What's the rationale and assumptions behind it.

Isn't it just a series of training and re training the EA in many windows of time/opportunity. In another words, many IS training and re-testing it in the next window of time OS and repeat the process several times/continuously.

1st of all, we assuming that if EA is re-trained many times in many windows/duration, it means that EA is robust? But isn't we re-training our EA to fit into that particular window/segment/duration. How does that make it robust to fit into other windows? We are just repeating the process again and again to fit into the latest window/segment. What make we think it will survive the overall duration?

Isn't that similar to Sleytus method of once a while, optimise his old EA to fit into the most recent window/segment of data?

I think there are two process we need to be mindful of Training and Testing. But often, they are done together, we lose sight of our intention.

In training, I would like to train my EA to handle a specific window of data (the focus in not the duration of the data, the focus is what type of market conditions within that trading period). For example, If I develop Trending EA, I would like to optimise my Trending EA in a Ranging data, to train my EA to fine tune their parameters better to avoid false signals.

After training/optimising my EA, I would like to subject it to Testing. That's where I would like to choose as long as possible the historical data to see how long can this EA survive in various market conditions.

Hence, in my limited understanding of Walk Forward, I personally feel it's just a repetitive training process without any particular intention in mind what kind of EA we are intending to train. Hence, we get a jack of all trade EA, but a master of none, it's neither a ranging EA nor a trending EA and thus I doubt how good can the results be. Bear in mind, it's just my opinion. I would still like to do more Walk Forward testing to see whether the results fits into my assumptions. And to see how valuable Walk Forward really are. Opinions are just opinion, until it's tested, it would be just a presumptions.