Re: HFMarkets (hfm.com): Market analysis services.

Date: 18th December 2023.

Market Recap: Focal BoJ ahead & the very last key US data

Markets are starting to wind down for the year. The four major central bank, the FOMC, ECB, BoE, and SNB all left policy rates unchanged, and most dialed back their hawkish biases. But while officials tried to jawbone and push back that early rate cuts are not on the table, the markets quickly equated the steady stance and shift in bias to pricing in rate cuts sooner than later. Indeed the markets ran with expectations for easing as soon as the first half of the year, if not March for the FOMC.

Economic Indicators & Central Banks:

*FED: Fed’s Bostic sees two 25 bp cuts in 2024, but said it’s not an “imminent thing,” in a Reuters interview. New York Fed President Williams said its too early to begin thinking about cuts. Still, U.S. futures are already finding buyers again after a mixed close on Wall Street Friday.

*Japan: The BoJ is the focal point this week as it’s the last major bank to meet. Risks for no action have picked up as data have failed to give Governor Ueda the confidence needed to exit negative rates or YCC at this point.

*China’s PBOC resumes 14-day cash injections. The move likely designed to smooth liquidity conditions over the year-end. Borrowing costs were held unchanged at 1.8% and 1.95% respectively.

Market Trends:

*Treasury yields slightly higher however the 2-year still closed the week with 28 bp drop, marking the lowest closing since mid-May. The 10-year notes stood at 3.91%.

*Asian stock markets declined, and European futures are also in the red, after Fed comments on Friday tried to push back against excessive rate cut speculation.

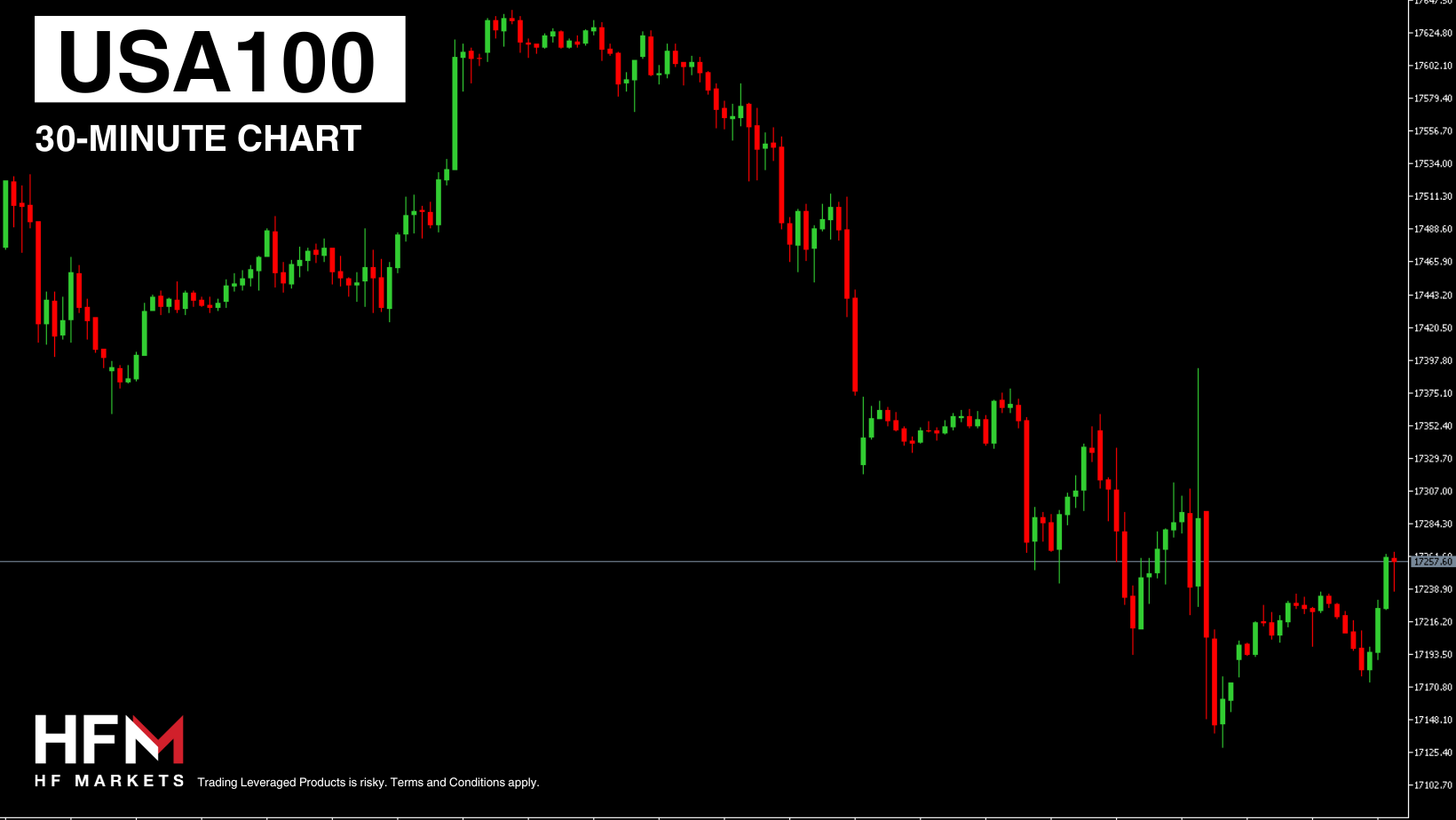

*Stocks: The JPN225 slumped 0.7% on weakness in Yen. The US500 futures inched up 0.3%, while US100 added 0.2%, EU50 futures slipped 0.3% and UK100 at 0.1%.

Financial Markets Performance:

*The USDIndex at 102.00 after drifting to 101.43.

*EURUSD corrected to 1.0920 after a solid weekly gain If Eurozone activity fails to stabilize, Lagarde will be under pressure to change her tune and prepare for rate cuts earlier rather than later.

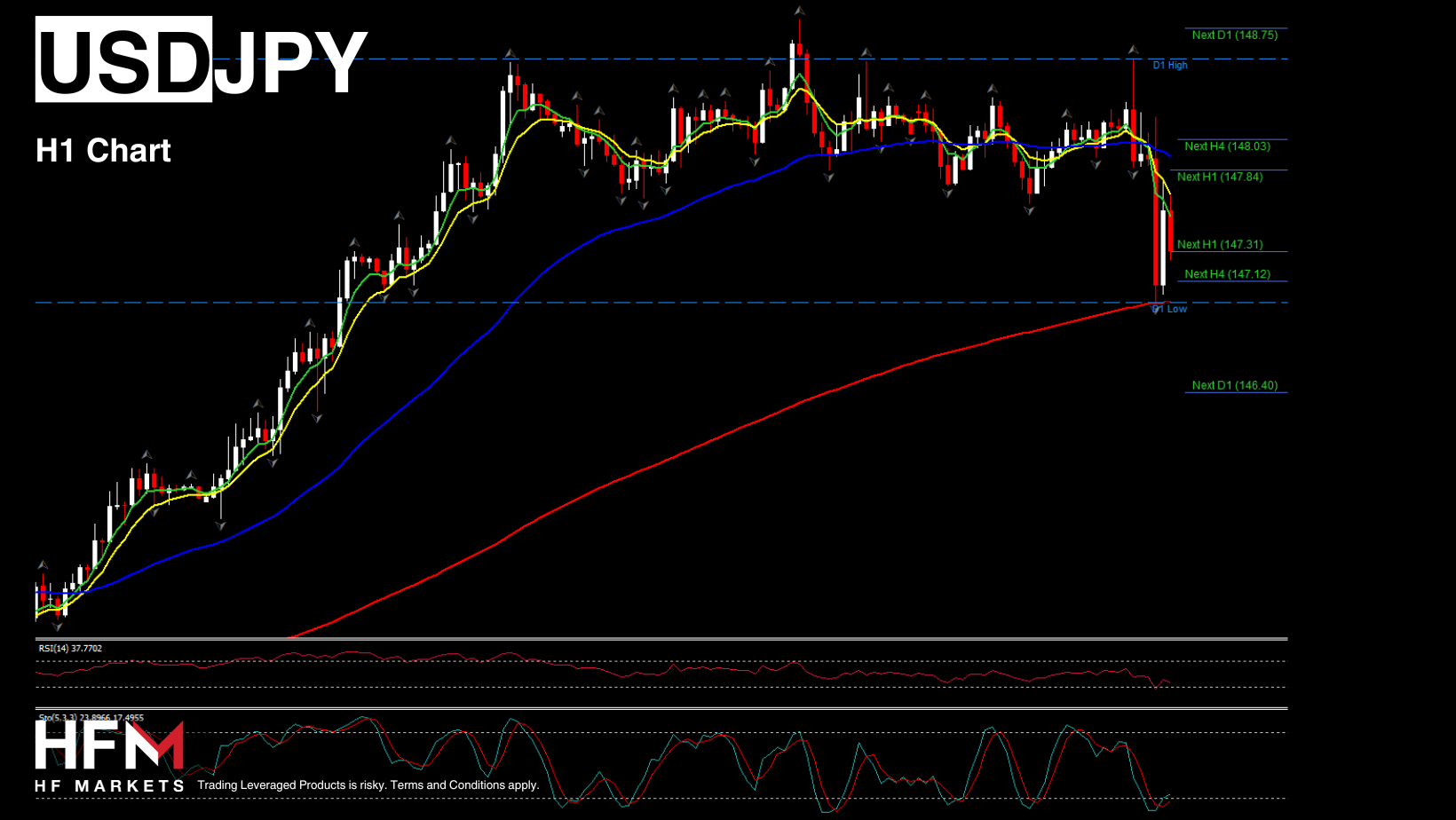

*GBPUSD moves sideways today and is at 1.2685, while USDJPY corrected again and is trading at 142.55 (38.2% Fib from 2023 upleg).

*Gold turned above $2000 as drop in the US dollar, yields and the Fed’s dovish pivot have helped to boost demand for the precious metal.

*Oil steadied above $72 after 5-month low last week amid worries supply will continue to outstrip demand. The weaker USD and dovish Fed comments helped to boost sentiment. The IEA said in its monthly report that it expects global oil consumption to rise by 1.1 million barrels a day in 2024, which means it has revised its demand forecast higher. That added further support and helped oil prices to at least stabilize over the second half of this week. Lower exports from Russia and attacks by the Houthis on ships in the Red Sea offered some support as well.

*Bitcoin holds above 40K for 11 day’s in a row, with increasing bullish bias.

*Key Mover: Goldman has raised year-end 2024 S&P 500 index target from 4700 to 5100, representing 8% upside from the current level. Decelerating inflation and Fed easing will keep real yields low and support a P/E multiple >19x.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Andria Pichidi

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.