Re: backtesting result is different from the real trading

Somebody else having this issue..?

Create and Test Forex Strategies

You are not logged in. Please login or register.

Forex Software → Expert Advisor Studio → backtesting result is different from the real trading

Somebody else having this issue..?

It's me.

My problem still exists. But it's from FSB not ea studio.

The strategy I show should open always position at time 0:00.

Even I have low latency, there are time delay about 0-5 mins before opening.

The result-testing in FSB

Backtesting result in mt4

Demo trade result

Demo trade result (The another broker)

I attach the strategy in this post. I'd like to know anyone will have the same problem like me?

If the entry times are correct in the MT backtest, it must be correct also on the real trading. A possible reason is to have execution restrictions, for example the trading may be suspended because of the swap calculations. Some ECN brokers do that. Please check if the broker quotes or trades between 00:00 and 00:05.

Hi, Popov

It seems backtest-result dont match perfectly with FSB.

You may see some order still taking late trigger. Is there some bug in the code?

Moonsky, you have 6 trades in the first demo and you are talking about "some" orders, which have late entry, when in fact it is only one trade, which is late couple of minutes? And when you check the calendar, you'd see it is Monday, which offers already an explanation.

Your second demo offers perfect - I repeat - perfect execution times and that leads me to believe your first demo broker is even below an ordinary bucket shop standard.

Therefore, pick your brokers carefully, teach yourself about trade sessions as well - real Asian session kicks off with Tokyo, before that it is a low liquidity/high spread borefest if you get my drift.

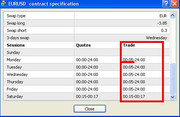

P.S. And always familiarize yourself with the terms and conditions your brokers offer you, an illustrating screenshot below.

Thank you,footon

I checked the trade session of second broker I show.The trading time begins at 00:05 as you said.

My some orders, I mean to lated opening order of first broker in strategy tester. I'm sorry for unclear question.

for the first broker,It begins at 00:00. The only one reason I know is requote. think like me?

I´ve just compared some of my last live trades today with the EA Studio backtest (feeding it the same data of course), I´ve got a perfect match down to a few points on the entry and exit prices (spread differences and slippage - just normal). If your strategies pass the mentioned MC tests, you should be fine (also in terms of starting bar, don´t forget that).

My Acceptance Criteria in Reactor mode totally depends on what I am looking for and how many years of data I am using. In general here is what I use *most* of the time on my 32 years H1 data set (all pairs):

Minimum R-Squared: 80 (want at least to have a *somewhat* acceptable curve in the initial strategy before handing it over to the Optimizer, as I don´t want to waste CPU power on the Optimizer for strategies that anyway will fail even after the Optimizer as their initial stage is too bad right from the start)

Minimum Trades: 1500 (now that could be much too much if using < 32 years of data, but for my huge set it´s the minimum I want to see because anything lower is not really statistically relevant)

Minimum Backtest Quality: 99 (obvious, right?)

That´s it already, nothing special.

geektrader, which Broker do you use? I'm looking for a good quality data broker and it seems to me that you have a very good one...

Forex Software → Expert Advisor Studio → backtesting result is different from the real trading

Powered by Forex Software Ltd.