I do it as follow.1.First you need a clean MT4 Backtest Installation. Make it as portable

So i add in my shortcut this.

M:\MT4Backtest\terminal.exe /portable /skipupdate

Than you are save that the MT4 Folder will always be same.

2. You need also from your Broker an MT4 Installation.

For example call it MT4Live and use same extensions in the terminal shortcut /portable

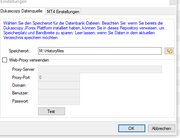

3. In Tickstory you set in settings the file where tickstory will put his downloaded files.

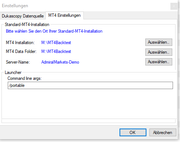

4. The Next Settings like in pic for the launcher. Here the Folder of your Backtest MT4 and add here also /portable in command as in pic. Now you have done all settings to get exported data to your MT4 Backtest Terminal.

5. Now you need to get your Broker Forex data like digits etc. which you get a script here. Put it into the MT4LIive experts Folder.

And attach this to a chart. Now you will get a file called xxx.mt4config.

6. In Tickstory choose your symbol right click export to mt4.

7. On Metatrader Info you now load the mt4config file to get the symbol specifications.

8. Choose your Start End date and check your timezone and now its downloading. Before close your MT4Vacktest Terminal

9. Now when is ready exported. Click on the symbol

Now your MT4Backtest Terminal is opening with only the Dukascopy charts in it.

10. To get this data for EA Studio download this script from eastudio

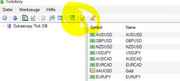

Once compiled you put it on your e.g exported EURUSD Chart and the script download the files, which you find in M:\MT4Backtest\MQL4\Files Folder.

Now you can upload it.

I hope it is clear.

The Problem is when you use tickstory with a connected demo account than you broker will overwrite the dukascopy backtest data everytime you run the terminal. So thats why you have to use a seperate mt4 install only for backtesting without beeing connected to a broker.

]]>